Rustat Report on Blockchain in the Real World

On 13 June 2019, this Rustat Conference brought together experts to explore the contemporary applications of, and future potential of, blockchain. Although cryptocurrencies – and especially Bitcoin – have captured public attention, the Conference aimed to also explore the other roles of blockchain and other distributed ledger technologies (DLT). We welcomed 43 participants from academia, the Civil Service, the Third Sector, industry, law, and the media in this one-day roundtable.

Across the last decade, some visionaries have claimed that blockchain would transform the world, disrupting business and financial practices, and ultimately our entire economic and political structures. Investors poured funds into crypto-tech and blockchain technologies. Others have observed, though, that the ‘bubbliness’ of the industry has led to many projects being touted as using blockchain, when in fact they do not. There is no doubt that there has been some exaggeration of the capabilities of the technology. Amongst this hype, our experts sought to explore what blockchain is and what it can currently be used for, as well as exploring potential future use cases.

While the experts held a range of views on most issues discussed, it was accepted by almost all our attendees that there needed to be better and more accurate consideration of blockchain by experts themselves and also by policy-makers. It was observed that there is extensive misunderstanding, cross-talk and confusion, which could have serious impacts on the appropriate regulation of the technology now and in the future. To address this, the day aimed to:

- define blockchain and distinguish hype from reality;

- explore cryptocurrencies and whether they are a real currency subsitute or a tool for speculation;

- detail the current non-financial uses of blockchain and detail real-world examples of use; and

- enquire what the future may hold, and how we might think about the role of regulation, both within industry and by governments.

We are grateful to our participants for their generosity in offering their time and expertise. A list of our experts who attended the Conference can be found here. The Agenda for discussion can be found here. As always with such deep and complex issues, the Conference raised more questions than it answered. The Conferences are conducted under a modified Chatham House Rule, which also applied to tweets from the day, and therefore only those willing to have material attributed to them have been quoted. The reports do reveal the identity and affiliation of speakers and participants, unless they requested otherwise.

We thank all those who attended, and in particular our Rustat Members for their ongoing support of the Conferences: They are currently Nick Chism, Dr James Dodd, Andreas Naumann, AstraZeneca, Harvey Nash and Laing O’Rourke.

What is blockchain?

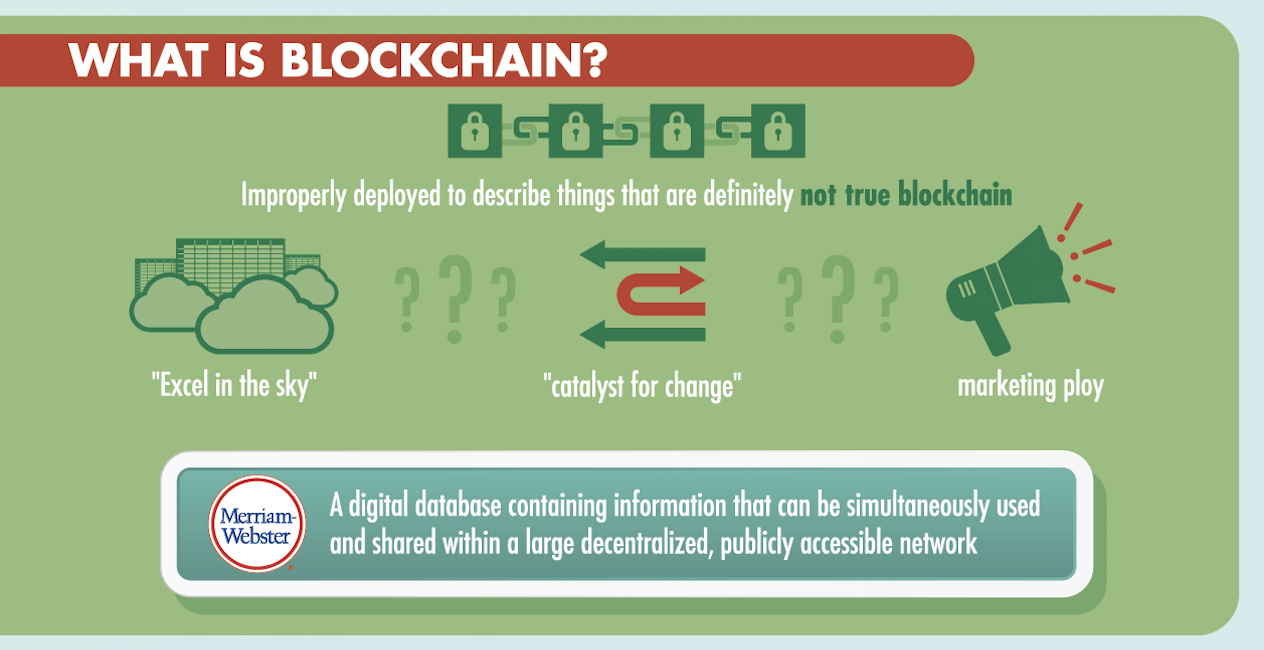

The first session of the day started by considering what blockchain actually is, and what the term is now taken to mean. As one attendee asked: "is it now a term used just to create hype with no actual real meaning?". Our experts began by observing that the word "blockchain" is often improperly deployed to describe things that are definitely not true blockchain. In many sectors, it is now used as a generalised term to refer to any distributed ledger technology – and in some cases there is an even wider definition used than that. Some at the Conference even went so far as to suggest the term was now meaningless, being used widely as a marketing ploy – or that it had become more of a belief system, or perhaps even a religion. It was noted that the ‘crytocraze’ has meant that simply mentioning the word ‘blockchain’ can be a significant bump to business valuations, at that as a result, it is now often merely an advertising and marketing tool, rather than describing any underlying technology.

DEFINING BLOCKCHAIN

‘A system in which a record of transactions made in bitcoin or another cryptocurrency are maintained across several computers that are linked in a peer-to-peer network.’ - Oxford English Dictionary

‘A growing list of records, called blocks, which are linked using cryptography. Each block contains a cryptographic hash of the previous block, a timestamp, and transaction data (generally represented as a Merkle tree).’- Wikipedia

‘A digital database containing information (such as records of financial transactions) that can be simultaneously used and shared within a large decentralized, publicly accessible network.’- Miriam Webster

However, there was agreement that while the term is often used unhelpfully, this doesn't preclude greater definitional clarity. Our experts sought to characterise it as being: 1) devised by multiple distributed parties who have come to a consensus based on pre-agreed rules ; 2) append-only; 3) a data structure containing records that are cryptographically linked. Although much public discussion of blockchain assumes that it must be public, it was highlighted that many of the uses are in fact private blockchains, which only trusted people can edit. However, some experts suggested these private blockchains were actually just shared databases. One expert amusingly quipped that blockchain is now just "Excel in the sky", which some concluded was in many ways a helpful explanation to the broader public.

Indeed, many of the experts noted that part of the misapprehension about blockchain derives from continued assertions that it is new, innovative, and peculiar, when in fact many of its elements and technologies have long existed. They hype around blockchain often makes it feel inaccessible, and therefore desirable to some, while frightening to many in the public at large. Our experts noted that many people on the street avoid cryptocurrencies, for example, because they don't understand and therefore fear them, rather than because they can't easily be used. It was noted that even some coffee shops in Cambridge take Bitcoin, but that other forms of payment tied to fiat currencies are preferred as they don't scare people as much; a point picked up again in the second session. Indeed, a core point our experts highlighted was the need for greater exploration of public understandings and social interactions around blockchain, demanding social scientists and humanities specialists be brought into discussions and research more extensively.

Discussion also considered blockchain as a consensus mechanism, arguing it was intended to replace the need for a central authority, like a government, that instead uses rules and incentives that keep members of the network truthful. This initiated heated debate over the underpinning ideology of such technology and regulation itself. While some saw blockchain as breaking down the traditional role of the state and markets, shaking up our systems, others saw the technology as a tool that like any other would need to be regulated to ensure it is used for the public good rather than profit for the few. While such deep philosophical questions were hardly resolvable in the time available, our experts noted that one of the greatest values of blockchain is that it catalyses such important underpinning discussions.

Indeed, some experts noted that blockchain hype can enable other benefits. For example, one participant noted that the drive in some companies to look to blockchain as a solution gets the organisation to talk about how to actually address the underpinning challenges, which are often involve process redesign, not blockchain. One expert termed blockchain a "progenitor for change", arguing that often only something as simple as SSL certificates or improved robotic processes were needed, but that the blockchain buzz often starts that conversation.

Others, though, were eager to pin blockchain down further, to allow proper discussion of the negative consequences that there could be, and regulation that may be needed. Trust was highlighted as a critical concept. The immutability of blockchain is one way to foster trust, but there is also a need to trust what is going into the chain, and what the purposes are. This led experts in the following sessions to explore more fully how blockchain can be used and why regulation may be desirable.

Are cryptocurrencies a real currency?

In the next session, our experts considered cryptocurrencies, exploring whether they are a tool for speculation or whether they are a real currency substitute. Much of the discussion considered the state of affairs around cryptocurrencies and the problems they currently pose both to the economy and for everyday use. Indeed, our experts were quick to note that the growing buzz around cryptocurrencies had created a vulnerability to scams.

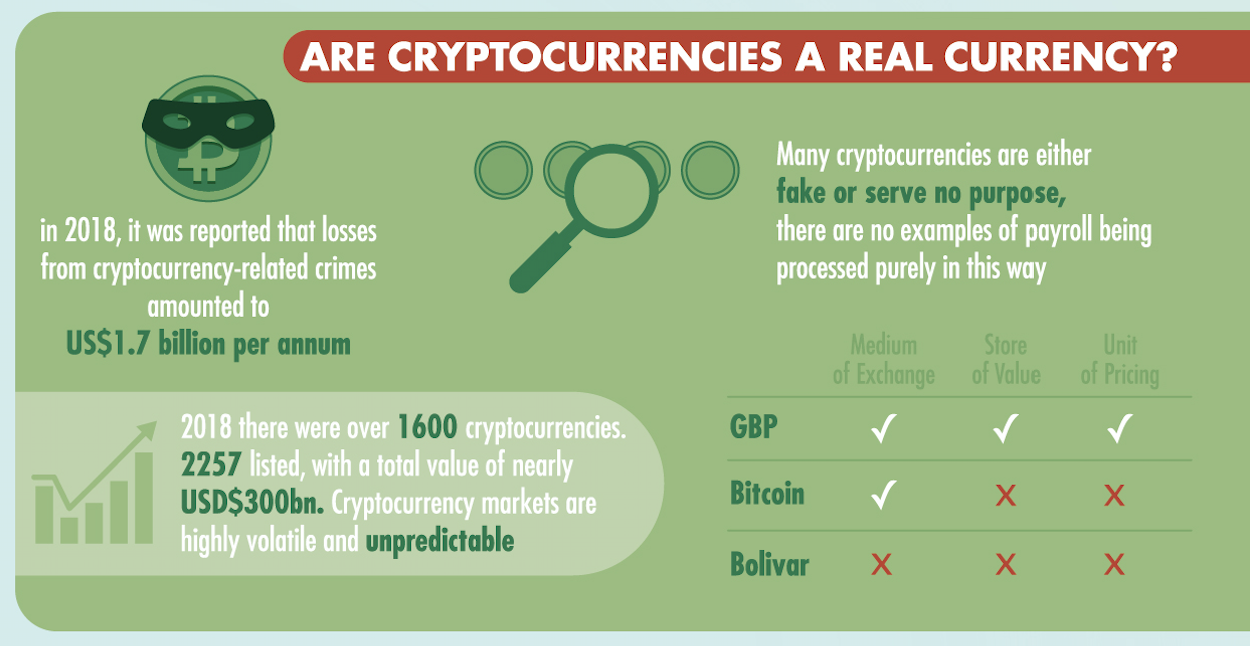

One expert noted that in 2018 there were over 1600 cryptocurrencies. Another expert cited that there are currently 2257 listed, with a total value of nearly USD$300bn. The disagreement in numbers in part traces to the fact that many cryptocurrencies are either fake or serve no purpose. Indeed, in 2018, it was reported that losses from cryptocurrency-related crimes amounted to US$1.7 billion per annum. Meanwhile, another expert noted that bids for setting up a cryptocurrency system in one Chinese city produced over 120,000 proposed currencies of which only 197 were verified as true companies. Our attendees warned that potential investors should be very careful to research what they’re putting their money into. It was also suggested that people take on a lot of risk when they step out of the regulated world of fiat currencies. It was also suggested that in order to protect consumers several things must take place around crytpocurrencies, including the development of a taxonomy or cryptocurrencies, and a grading system, amongst other things.

Our experts also raised the confusion over what cryptocurrencies actually are. Debate began with the question: are cryptocurrencies just digital forms of fiat currency? One expert noted that Bitcoin, for instance, was starting to look a lot more like an asset than a true currency. This led our experts to define what a currency actually is. The factors set out for being a currency were: 1) that there is a medium for exchange; 2) that people can receive it and change it for value, using it over time; and 3) that is used as a unit for pricing. Examples were used to highlight how these criteria might be applied. The British Pound does well against all three criteria, whereas Bitcoin fails as a unit of pricing; people convert Bitcoin over to dollars or pounds, rather than valuing things in Bitcoin itself. It was also noted that some fiat currencies fail these tests – the Venezuelan Bolivar fails all three.

Some suggested that bitcoin is better regarded as either a utility token or security token, as opposed to a currency. It was not yet clear whether or not Bitcoin, for example, will become a major store of value like gold or even a new global reserve currency like the US dollar – although some would clearly like it to displace fiat currencies. However, even as a token, there are limits – like company scrip or green shield stamps, it results in locked spending. It was noted that while a few organisations offer to pay in cryptocurrency – such as Facebook and its new coin offer – there were no examples of payroll being processed purely in this way.

It was also noted that cryptocurrency markets are highly volatile and unpredictable, with particular concerns about the reliability and security of exchanges – it matters little how robust a cryptocurrency is in itself, if there is no security over exchange. The volatility is also a major challenge to cryptocurrencies as currencies – if the value is expected to go up, it would not be rational to ever spend them; and if it is expected do decline, it would not be rational to accept them.

Technical problems also arise for the everyday use of cryptocurrencies, such as the very limited bandwidth available globally for transactions, meaning it can take a long time to process any payment. Additionally, for most implementations, someone with sufficient control of the currency (typically >50%) could control the consensus chain, making changes as they wished. It is notable that the wealth is also centralised. Using a Gini coefficient (where 1.0 means that a single person controls 100% of income/wealth), North Korea scores 0.86, the United States scores 0.41, while Bitcoin scores 0.88.

There are some advantages to the use of cryptocurrencies – in places such as Venezuela, they are more stable than the local fiat currency, and so are considerably more attractive. The same is true of countries where there are strong controls on capital export. Some of our experts noted that there are opportunities to bypass banking systems, and hence achieve large savings on transactions such as issuing debt. It was suggested that further disruption of the banking system could be beneficial, if handled correctly. Notably, the current valuation of all cryptocurrencies is not large compared to global financial markets, reducing the risk of large-scale instability.

There was extensive discussion on the philosophy underpinning cryptocurrencies, leading our experts to question our understandings of finance and also to suggest that we would need to revisit fundamental economic theory to cope with the new opportunities and challenges they present.

What are the current non-financial uses of blockchain?

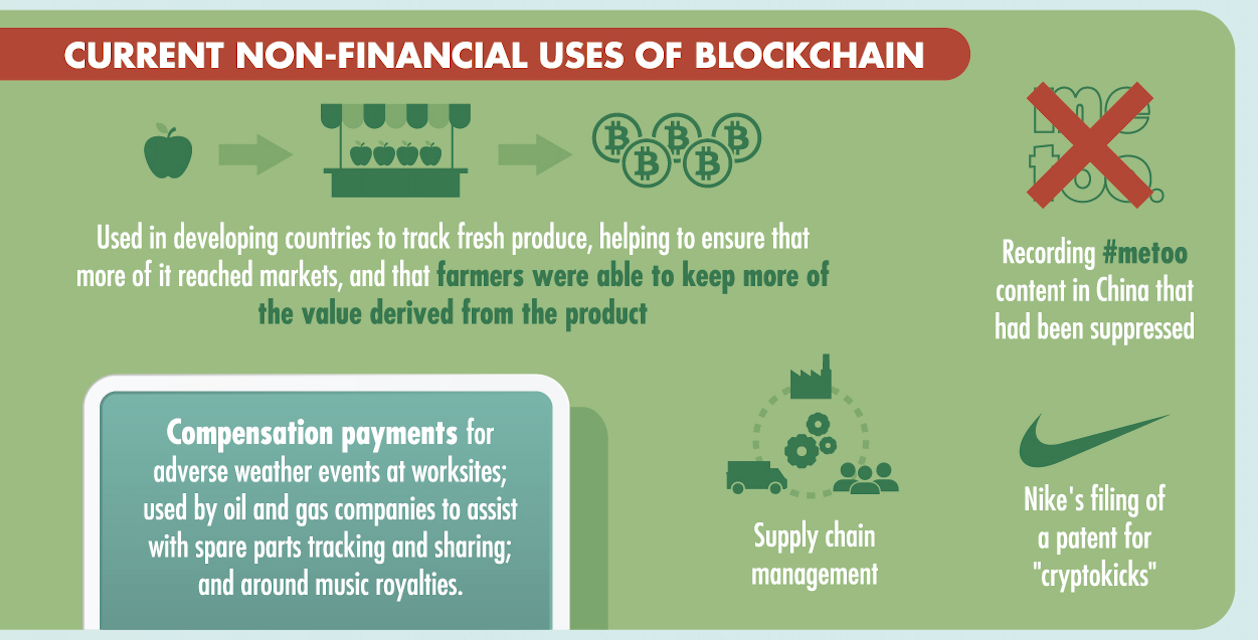

The third session considered the current non-financial uses for blockchain technologies, including specifically how the technology can be used to create and mediate value chains. One attendee highlighted how blockchain is being used in developing countries to track fresh produce, helping to ensure that more of it reached markets, and that farmers were able to keep more of the value derived from the product. Using a distributed ledger system meant that individual products could be easily tracked at every stage in the process, allowing farmers greater visibility of what was happening to their produce, and allowing consumers to check provenance and how costs were being allocated, bringing greater trust and transparency to the system. It was suggested that farmers could, for instance, earn 10 times more than they had previously by using these technologies. It was pointed out, however, that any such system can only be as good as the accuracy of the original labelling of the goods – efforts to monitor the provenance of high-quality wine by tagging the corks could be defeated simply by putting the corks into bottles containing cheaper wine in the first place.

Other uses than supply chain management were also considered. One expert highlighted the potential for blockchain to have a key role in fostering political dissent. The example given considered how #metoo content in China had been suppressed, leading some users to make use of the immutability property of blockchain to allow allegations to be recorded publicly and more permanently, with the state being unable to remove them directly. One expert argued that blockchain had liberatory potential, and that it would be a powerful tool in disrupting and replacing dysfunctional, authoritarian, or corrupt governance systems.

Some proposed uses were considered to be rather questionable, such as a consent tracking application that had been recently launched that sought to log and verify mutuality of consent at various stages of a relationship. The experts were quick to note that such use of blockchain for individual histories and personal approaches posed real issues in understanding and responding to privacy and also around the permanency of testimony. Permanence has some advantages, but in other cases it was felt to be important that some data should be editable, and records erased. Examples given were around criminal histories, where a juvenile might need to have a record expunged, where a person is exonerated, or where a crime is retrospectively removed from the books and previous convictions erased, like has happened around interracial marriage, legalisation of cannabis use, and homosexuality.

There were several discussions about the role that blockchain could play in establishing identity and verifying educational or other status. One example raised was projects that sought to deploy the technology to help refugees. Experts set out how various projects have sought to use DLT to create immutable records of identity and personal data, as well as a history of relevant transactions, that could support applications for refugee status. It was highlighted that in storing information like biometric data in a decentralised, immutable form like the blockchain there is the possibility to actually deprive the individual from access by removing their key, and for the information to be used in ways that cannot be controlled by those who supplied the data. These concerns mirrored existing observations by those in global human movement research.

There was also discussion over the underpinning question of identity. In particular, should people or organisations be tied to having precisely one digital identity. Doing so enables various rights to be appropriately distributed – such as food rations in a refugee camp – but also imposes very strong constraints on privacy and freedom of expression.

Other use cases highlighted included how blockchain could be used to automate currently complex processes, such as compensation payments for adverse weather events at worksites; used by oil and gas companies to assist with spare parts tracking and sharing; and around music royalties. The underlying objective in these cases was to use these technologies to increase process efficiency.

Tokenisation to modify or incentivise behaviour was also discussed. Our experts noted that Nike's filing of a patent for "cryptokicks", which suggests the company plans to use crypto wallets, including tokens, in an online marketplace. While the experts couldn't say exactly how Nike planned to use cryptocurrency, it was noted that tokenisation was a growing feature as companies come to create their own cryptocurrencies to allow purchases within a created ecosystem.

The Future of Blockchain and Regulation

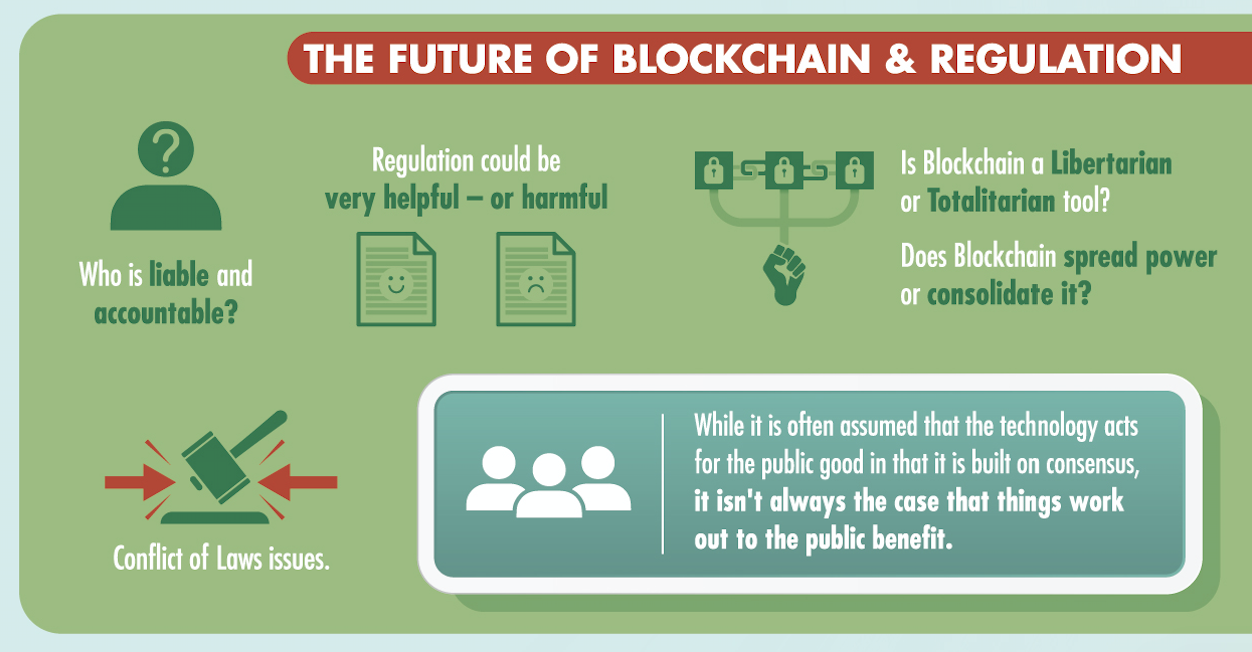

In the final session, the experts considered how we might set up an enabling structure to regulate future developments around blockchain. Although some felt that one of the benefits of blockchain was that it was hard to regulate, most felt that regulation was important, if challenging. As well as technical challenges, there are difficulties that arise from the cross-jurisdictional nature of the arrangements most commonly involved in blockchain uses. It was highlighted how cryptocurrencies and blockchain around supply chain in particular involve cross-border features, and that this necessarily creates Conflict of Laws issues. Who owns what and where? Are cryptocurrencies possessions Where is the seat of dispute resolution? It was highlighted that these issues continue to be unresolved.

Second, it was highlighted that cryptocurrencies present issues about who is liable and accountable. One example given was that if there was a hard fork in Ethereum at some time, after all the nodes and chain had upgraded, if an individual had assets based on the old chain that did not transfer across, these could just disappear. If this did happen, who would be liable and subject to claim: the developers? the hard fork proposers?

Beyond practical legal issues, the experts also raised extensive ethical and governance problems that must be addressed. The experts highlighted the ways in which blockchain makes us need to consider the changing role of public and private actors and different roles and responsibilities in regulation. It was noted that blockchain is heavily regulated by internal rules and processes – possibly even too tightly, in that it could be very difficult to undo errors. However, controls elsewhere in the ecosystem were generally very light.

There was considerable discussion about the speed of change. One expert emphasised that there is often an attitude that agile is the right way to go, but that this can lead to doing things too fast and without enough thought. Thus, while it is often assumed that the technology acts for the public good in that it is built on consensus, it isn't always the case that things work out to the public benefit.

As a result, the experts called for more detailed thinking about what might be possible and what might go wrong. Perspectives on the role of regulation in the sector were greatly varied. Some advocated for anarchy in the digital sense, suggesting that this approach allowed for innovation and swift development of new ideas. Others were concerned about regulating poor conduct and unethical developments.

Experts also called for reconsideration of all our economic models, as it was highlighted how in terms of cryptocurrencies many market economics don’t fully apply. Indeed, it was pointed out that distributed autonomous organisations are blurring the lines around the way that people are working and transacting, resulting in changes on a microeconomic level.